Strategic Accounting for Construction Change Orders: Protecting Your 2026 Profit Margins

- Wendy Okie

- 3 days ago

- 12 min read

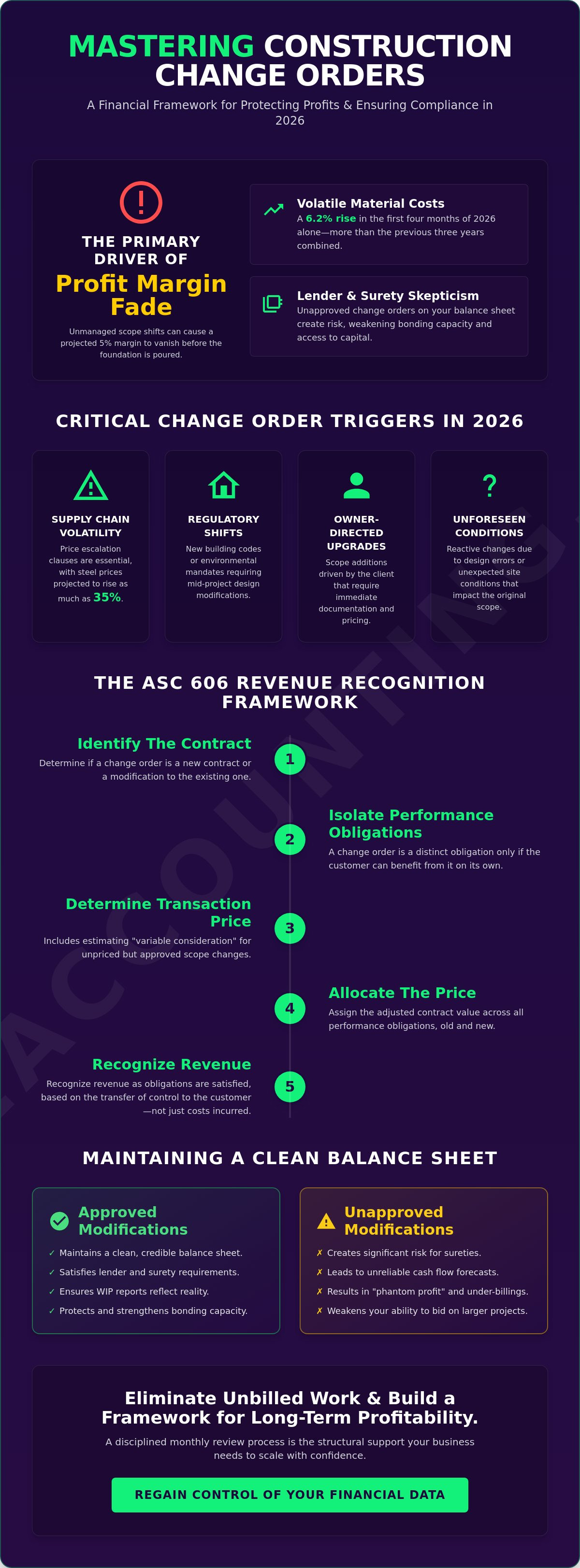

Did you know that the first four months of 2026 saw a 6.2% rise in material costs, which is more than the cumulative increase of the previous three years combined? This volatility means that even a minor delay in documenting scope shifts can lead to massive profit margin leakage. You're likely familiar with the stress of performing unbilled work while waiting for a signature, only to face skepticism from your surety or bank when those unapproved amounts hit your balance sheet. Mastering the technical side of accounting for construction change orders is no longer just a back-office task; it's a vital strategy for protecting your project's structural integrity.

We understand that the shift toward ASC 606 revenue recognition rules can feel like a moving target, especially when you're balancing historically high backlogs with a tightening labor market. This article provides a clear, disciplined framework to help you regain control over your financial data. You'll learn how to align your billing cycles with the transfer of control principle, transform unapproved claims into reliable revenue estimates, and produce the lender-ready statements required to scale your business with confidence through 2026.

Key Takeaways

Identify why change orders are legally binding financial events that represent the primary driver of profit margin fade in the current economic climate.

Master the five-step ASC 606 model to ensure your accounting for construction change orders accurately reflects when customers obtain control of the asset.

Distinguish between approved and unapproved modifications to maintain a clean balance sheet that satisfies lender and surety requirements.

Learn how to optimize QuickBooks job costing by setting up specific items and estimates that capture the true cost of contract modifications.

Implement a disciplined monthly review process to eliminate unbilled work and build a structural framework for long-term project profitability.

Understanding Construction Change Orders as Financial Events

A change order is much more than a signature on a job site. It's a legally binding amendment that alters the original contract's price, scope, or timeline. When you're asking What is a Change Order? from a financial perspective, you're really asking how to recalibrate your project's entire economic foundation. In 2026, these documents are your primary defense against "margin fade." This phenomenon occurs when actual costs slowly erode projected profit, often because field changes weren't properly reflected in your accounting for construction change orders. Without a disciplined framework, a 5% margin can vanish before the foundation is even poured.

Financial credibility depends on how you categorize these events. Scope changes are often owner-driven additions, while unforeseen conditions or design errors are reactive. Each requires a different narrative when presenting data to lenders. Sureties look for structural integrity in your reporting. If they see a pattern of "unapproved" changes stacking up, they see risk. They want to know that your financial statements reflect reality, not just optimism. Proper management ensures that your bonding capacity remains intact, allowing you to bid on the high-demand data center and infrastructure projects driving the 2026 market.

Beyond Scope: The Impact on WIP and Cash Flow

Every change order shifts your Estimated Cost at Completion (EAC). If you don't update your Work-in-Progress (WIP) report immediately, you risk significant under-billings. This creates a "phantom" profit on paper that doesn't exist in your bank account. When unrecorded changes accumulate, your monthly cash flow forecasting becomes unreliable. This lack of clarity is exactly why banks become hesitant. Establishing a rigorous system for accounting for construction change orders ensures that your billing stays ahead of your costs. Utilizing Fractional Controller Services can provide the high-level oversight needed to synchronize field production with back-office reporting.

Common Triggers for Change Orders in 2026

The current market presents unique challenges that demand proactive cost management. Supply chain volatility is no longer an outlier. With material prices for steel projected to rise as much as 35% in 2026, price escalation clauses are essential triggers for contract modifications. You'll likely face regulatory shifts as well. New building codes or environmental mandates often require design modifications mid-project. Whether it's an owner-directed upgrade or a necessity-driven field change, treating these as minor administrative tasks is a mistake. They are critical financial pivots that dictate the long-term health of your business.

The Revenue Recognition Framework: Navigating ASC 606

The transition to ASC 606 has fundamentally altered the landscape for private construction firms. By 2026, the focus has shifted entirely from just tracking costs to identifying when a customer obtains control of the asset. This five-step model requires a refined approach to accounting for construction change orders to ensure your financial statements reflect the economic reality of your projects. You must identify the contract, isolate the performance obligations, determine the transaction price, allocate that price, and finally recognize revenue as those obligations are satisfied. Skipping these steps often leads to revenue reversals that can devastate your year-end margins.

Determining whether a change order is a separate contract or a modification of the existing one is a critical first step. If the additional work is distinct and priced at its standalone selling price, it's a new contract. However, most construction changes are integrated into the original scope, meaning they are modifications. This distinction dictates whether you record revenue prospectively or through a cumulative catch-up adjustment. If you feel your current systems lack this level of precision, you might consider a discovery call to evaluate your structural framework.

Contract Modifications and Performance Obligations

A change order creates a distinct performance obligation only if the customer can benefit from the good or service on its own. In most structural projects, changes are highly interrelated with the original work. When this happens, you must perform a cumulative catch-up adjustment. This recalibrates your revenue based on the new total contract value and your updated percentage of completion. In 2026, ASC 606 dictates that construction contract modifications must be evaluated based on the transfer of control to the customer rather than simply the incurrence of costs.

Estimating the Price of Unpriced Changes

Accounting for construction change orders becomes particularly complex when the scope is approved but the price is not. This is known as "variable consideration." To include these amounts in your contract price, it must be probable that a significant revenue reversal will not occur. You generally choose between the "most likely amount" method, ideal for single-outcome claims, or the "expected value" method, which uses a probability-weighted average for complex disputes. Relying on conservative estimates protects your financial credibility with sureties. It ensures you aren't recognizing "phantom" income that could vanish if a claim is eventually denied by the owner.

Accounting for Approved vs. Unapproved Change Orders

The distinction between an approved change order and an unapproved claim is the difference between a secure profit and a speculative asset. From a reporting perspective, these two categories exist in entirely different worlds. Approved changes are legally settled amendments that provide the certainty required for accurate management accounting. Unapproved changes, however, are essentially "claims" that carry significant risk of revenue reversal. Maintaining precise accounting for construction change orders requires a binary approach to ensure your balance sheet doesn't become inflated with phantom income that a lender or surety will eventually discount.

Sureties and banks view these categories through the lens of liquidity and risk. An approved change order is seen as a reliable increase in contract value. In contrast, unapproved claims are often viewed with skepticism. If your financial statements show a high volume of unapproved work, a surety may exclude those amounts from your working capital calculations. This directly impacts your bonding capacity and your ability to secure the large-scale projects that define the 2026 market. Documentation is your only defense; if a change isn't backed by a clear paper trail, it doesn't exist in the eyes of an auditor.

Recording Approved Change Orders for Financial Credibility

When a change order is signed, you must update both the total contract value and the estimated costs at completion simultaneously. This synchronization ensures your percentage of completion remains accurate and your profit margins stay protected. You should always secure a signature before billing for additional work. Doing so avoids the disputes that lead to aged receivables and strained client relationships. From a strategic standpoint, approved changes strengthen your debt-to-equity ratio by increasing recognized revenue and equity without increasing liabilities. It's a hallmark of a disciplined, well-managed construction firm.

The Danger of Unapproved and Unpriced Claims

GAAP allows for the recognition of revenue on unapproved work only if it's "probable and estimable." This is a high bar to clear. You must demonstrate that the owner is likely to pay and that you can reliably calculate the amount. Most conservative firms choose to wait for written approval before adjusting the contract price in their books. If you record unbilled revenue for unapproved work, it sits on your balance sheet as "Costs in Excess of Billings." While this is an asset, a high CIEB balance is a red flag for lenders. It suggests you're funding the owner's project with your own cash flow, which creates a structural vulnerability in your business.

Best Practices for Job Costing Change Orders in QuickBooks

Managing the technical side of accounting for construction change orders requires more than just administrative diligence; it demands a structured software environment. QuickBooks serves as the nerve center for your project data, but its effectiveness depends entirely on your initial configuration. If your items aren't mapped correctly, your profit reports will be distorted, leading to the margin fade discussed in previous sections. Establishing a standardized naming convention, such as "CO-001: [Description]," creates a clear audit trail that lenders and sureties expect in 2026. This level of organization transforms your software from a simple ledger into a strategic tool for project oversight.

Setting Up Change Order Items and Sub-items

To track changes effectively, you should create parent-child relationships within your item list. By setting up a parent item for the original contract and sub-items for each modification, you can view the financial health of the base bid and individual changes separately. It's vital to map these change order income items to the correct general ledger accounts to ensure your financial reporting remains accurate. For a deeper dive into software optimization, consult our guide on Mastering QuickBooks for Contractors. If you find your current setup is creating more confusion than clarity, you can schedule a discovery call to discuss our specialized QuickBooks Setup & Training services.

Tracking Costs Against the Revised Budget

The "Project" center in QuickBooks Online is essential for comparing your actual costs against revised estimates in real time. When a change order is approved, you must update the project estimate to reflect the new scope and budget. This allows you to run a "Job Profitability" report that accounts for the total modified contract value rather than just the initial bid. To maintain granular visibility, you must link every vendor bill to a specific change order line item using the "Customer/Project" column in the transaction window. This practice prevents costs from being lost in the general project bucket, ensuring that every dollar spent is accounted for and billed correctly.

Consistent tagging is the only way to ensure your cash flow forecasting remains reliable as material prices continue to fluctuate. We recommend a monthly reconciliation of your "Estimate vs. Actual" reports to catch any unbilled work before it impacts your bottom line. Following these steps ensures your structural framework remains sound:

Standardize: Use a consistent numbering system (CO-001, CO-002) for every modification.

Synchronize: Update the QuickBooks estimate as soon as the change is approved.

Isolate: Use sub-items to keep change order costs separate from the original contract scope.

Review: Compare job profitability weekly to identify potential overruns early.

Protecting Profit Margins with Strategic Financial Oversight

Software and systems provide the foundation, but strategic oversight is what secures your profit. Even the most precise QuickBooks setup can't protect your margins if your team lacks a disciplined review process. A monthly financial review is your most effective tool for catching unbilled work before it becomes a permanent loss. By analyzing the delta between your estimated costs and actual spend, you can identify scope creep that hasn't been formalized into a change order. This proactive approach to accounting for construction change orders ensures that your 2026 profit margins remain insulated from the material and labor volatility currently impacting the industry.

Transitioning from reactive bookkeeping to proactive financial leadership requires a shift in perspective. You aren't just recording history; you're managing future outcomes. When you treat every project modification as a strategic financial event, you build a business that is resilient and lender-ready. This level of maturity is what distinguishes a growing contractor from one that is merely surviving. It requires a commitment to structural integrity in your data that matches the integrity of your physical builds.

The Role of a Fractional Controller in Change Management

A disciplined controller transforms your Work-in-Progress (WIP) schedule from a static report into a dynamic roadmap for profitability. They provide the high-level oversight necessary to ensure that your accounting for construction change orders is GAAP compliant and satisfies the rigorous demands of sureties. By reviewing your WIP schedule for accuracy, a controller identifies potential claims early, allowing you to address them with the owner before they escalate into legal disputes. This specialized guidance is a core component of our Construction Bookkeeping Services, which focus on building a scalable financial infrastructure for your firm.

Building a Change Order Policy for Long-Term Stability

Protecting your bottom line requires a clear, enforceable "Change Order Policy" that bridges the gap between the field and the office. This policy should establish a non-negotiable "no work without a signature" rule for any scope changes that aren't necessity-driven field emergencies. When your project managers understand that documentation is as critical as the work itself, you eliminate the ambiguity that leads to uncollectible revenue. Standardizing this workflow ensures that every modification is captured, priced, and billed according to the framework we've established in this guide.

To truly master your project-based financial tracking, you need a partner who understands the mechanics of your specific market. We help you move beyond basic administrative tasks to construct a comprehensive structural framework for your business. If you're ready to secure your financial future, partner with Okie Accounting Group LLC for Fractional Controller Services today.

Define: Clearly outline what constitutes a change order versus a field fix.

Authorize: Designate specific personnel who have the authority to sign off on cost increases.

Document: Require immediate photographic or written evidence of unforeseen conditions.

Review: Conduct a joint field-and-office meeting every 30 days to reconcile unbilled work.

Building a Resilient Financial Foundation for 2026

Mastering the complexities of ASC 606 and rigorous QuickBooks job costing is no longer optional for contractors who want to thrive. By treating every modification as a critical financial event, you protect your business from margin fade and build the lender credibility necessary for growth. A disciplined approach to accounting for construction change orders ensures that your financial statements reflect the structural integrity of your projects. We specialize in the construction and real estate sectors, providing nationwide strategic financial oversight as QuickBooks Online Certified ProAdvisors. Our framework moves you from reactive bookkeeping to proactive leadership, giving you total control over your project data.

You don't have to manage these technical hurdles alone. Our team acts as a strategic partner, helping you build foundational systems that secure long-term stability and profit. If you're ready to transform your financial reporting into a tool for growth, Gain Financial Clarity with Specialized Fractional Controller Services today. Your commitment to accuracy today is the best insurance for your profitability tomorrow.

Frequently Asked Questions

What is the difference between a change order and a construction change directive (CCD)?

A change order is a bilateral agreement where both the owner and contractor agree on the scope, price, and schedule adjustments. In contrast, a Construction Change Directive (CCD) is a unilateral order from the owner directing you to proceed with work before an agreement on cost or time is reached. CCDs often lead to financial claims because the final compensation remains unsettled while you're already incurring project costs.

How do I record a change order in QuickBooks Online for a construction project?

You should record a change order in QuickBooks Online by updating the existing project estimate or creating a new estimate linked to the same project. Add specific line items for the additional work and ensure they're tagged to the correct sub-items for granular tracking. This practice ensures your "Estimate vs. Actual" reports remain accurate and reflect the true, modified contract value at any given time.

When can I recognize revenue for an unapproved change order under ASC 606?

Under ASC 606, you can only recognize revenue for an unapproved change order if it's probable that a significant reversal of recognized revenue won't occur once the uncertainty is resolved. This requires a high degree of certainty that the owner will pay and that you can reliably estimate the amount. Most firms use the "most likely amount" method for single-outcome claims to maintain conservative and reliable financial reporting.

How do change orders affect my Work-in-Progress (WIP) schedule?

Change orders directly impact your Work-in-Progress (WIP) schedule by increasing both the total contract value and the estimated costs at completion. If you fail to update these figures simultaneously, your percentage of completion will be skewed, leading to misleading over-billings or under-billings. Accurate accounting for construction change orders is essential for maintaining a WIP report that truly reflects the current profitability of your projects.

What are the common causes of change orders in 2026?

In 2026, the primary triggers for change orders include extreme material price volatility and mid-project regulatory shifts in building codes. Supply chain disruptions often require substitutions that alter the original design or cost structure. Additionally, the ongoing labor shortage sometimes necessitates schedule extensions or shifts in construction methodology that must be formalized through contract amendments to protect your bottom line.

How should I price a change order to ensure I maintain my profit margin?

To protect your profit margin, you must price change orders using your fully burdened labor rates and current material costs. Don't forget to include overhead allocations and a profit markup that matches or exceeds your base bid. Since material costs for steel and lumber have seen significant double-digit increases in 2026, using real-time pricing data is critical for preventing margin erosion on additional scope.

Why do banks and sureties care so much about how I account for change orders?

Banks and sureties scrutinize your accounting for construction change orders because it serves as a litmus test for your financial discipline and risk management. High levels of unapproved changes suggest you're self-funding the owner’s project, which increases your risk profile and decreases your liquidity. They want to see a clean balance sheet where recognized revenue is backed by signed, legally binding agreements.

Can I bill for a change order before it is signed by the project owner?

You generally shouldn't bill for a change order before it's signed by the project owner unless your contract contains a specific provision for interim billing on CCDs. Billing for unapproved work often leads to aged accounts receivable and can strain your relationship with the owner. It's a best practice to secure a signature first to ensure that the payment is legally enforceable and undisputed.

Comments