Accounting for Cost-Plus Construction Contracts: A 2026 Strategic Guide

- Wendy Okie

- 3 days ago

- 12 min read

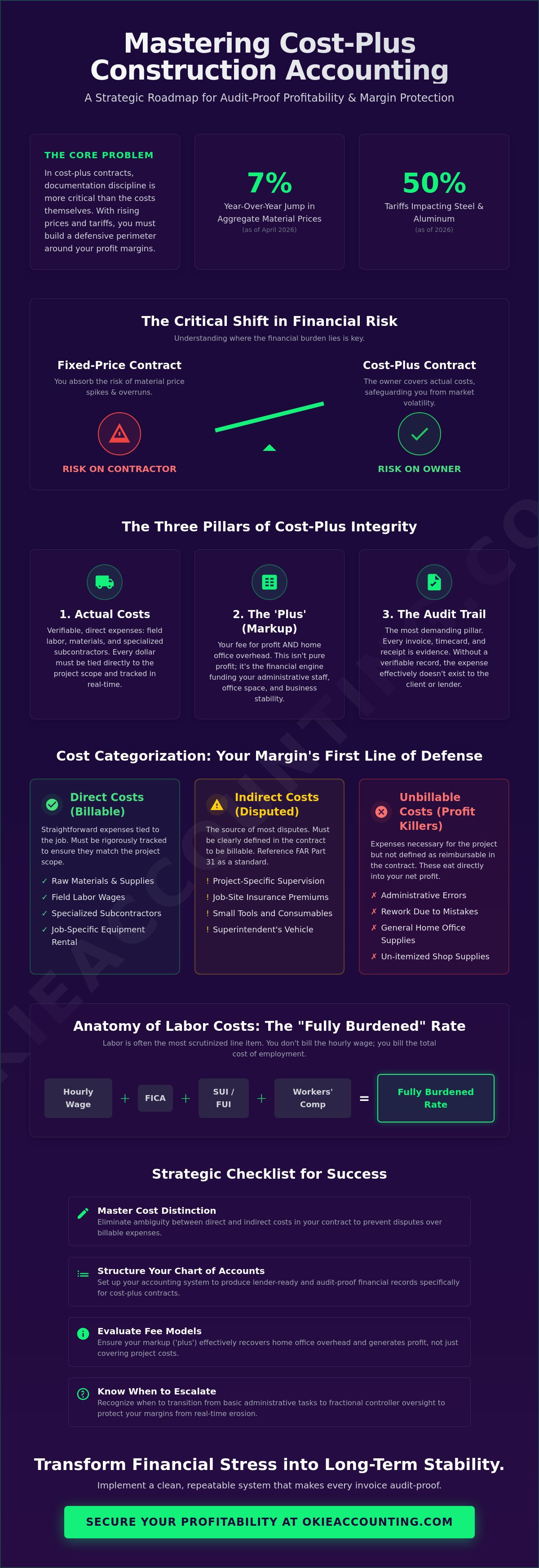

In cost-plus accounting, your documentation discipline is actually more important than the actual cost you're billing. It's a hard truth to face when aggregate material prices have jumped 7% year over year as of April 2026 and steel tariffs are sitting at 50%. You likely feel the constant pressure of justifying every line item to skeptical clients while trying to maintain your own structural integrity. Mastering the granular mechanics of accounting for cost-plus construction contracts isn't just about record-keeping; it's about building a defensive perimeter around your profit margins.

We understand that the administrative overhead of tracking billable versus non-billable items can feel like a second full-time job. This guide provides a strategic roadmap to help you implement a clean, repeatable system that ensures every dollar is accounted for and every invoice is audit-proof. You'll learn how to navigate ASC 606 nuances, handle the new $2,000 1099-NEC filing threshold, and utilize the latest 2026 software features. By the end of this article, you'll have the framework needed to transform your financial data from a source of stress into a tool for long-term stability and lender-ready transparency.

Key Takeaways

Identify the critical distinction between direct and indirect costs to eliminate ambiguity and prevent disputes over billable expenses.

Master the structural setup of your Chart of Accounts to ensure your accounting for cost-plus construction contracts produces lender-ready and audit-proof financial records.

Evaluate different fee models to ensure your markup effectively recovers home office overhead rather than just covering project-level costs.

Implement specific QuickBooks Online workflows, including the billable expense feature, to maintain a transparent and repeatable documentation system.

Recognize when to transition from basic administrative tasks to fractional controller oversight to protect your margins from real-time erosion.

Understanding the Accounting Framework of Cost-Plus Contracts

A Cost-plus contract is a pricing arrangement where the project owner agrees to reimburse the contractor for all actual project expenses, plus a predetermined fee for profit and overhead. In 2026, this model has become a vital safeguard against the 4% to 6% baseline inflation currently impacting the industry. While a fixed-price contract places the financial risk of material spikes on the contractor, the cost-plus framework moves that risk to the owner. This shift doesn't mean the contractor is off the hook. Instead, the focus moves from managing price to managing data. Accounting for cost-plus construction contracts requires a level of precision that generalist bookkeepers often overlook.

Cost-plus accounting is a transparency-first financial model that prioritizes the verification of expenditures over the simplicity of a fixed price. Trust is the primary currency in these agreements. If a client disputes a single line item, it can stall the entire payment cycle and damage the professional relationship. Establishing a disciplined management accounting system ensures that every dollar spent is backed by a verifiable record, protecting your reputation and your cash flow.

The Three Pillars of Cost-Plus Accounting

Managing these projects successfully relies on three foundational elements that must work in unison to maintain structural integrity:

Actual Costs: These are the verifiable expenses directly tied to the project scope, such as field labor, materials, and specialized subcontractors. With tariffs on steel and aluminum reaching 50% in 2026, these costs must be tracked and reported in real time to avoid billing lag.

The 'Plus' (Markup): This fee is designed to cover your home office overhead and net profit. It's vital to remember that the 'plus' isn't pure profit; it's the financial engine that funds your administrative staff, office space, and long-term stability.

The Audit Trail: This is the most demanding pillar of accounting for cost-plus construction contracts. Every invoice, timecard, and material receipt serves as the evidence required to satisfy client audits and lender requirements. Without a receipt, the expense effectively doesn't exist in the eyes of the owner.

Cost-Plus vs. Fixed-Price: The Bookkeeper's Perspective

From an operational standpoint, the biggest difference lies in how you track and report variances. In a fixed-price world, you're looking for ways to stay under a total price cap to protect your margin. In cost-plus, you're providing a narrative of the project's financial health through "estimate vs. actual" reporting. Revenue recognition also changes under the ASC 606 framework. You're generally recognizing revenue as you satisfy performance obligations, which is often tied directly to the costs you incur. This keeps your cash flow predictable, provided your billing cycle is tight and your documentation is impeccable.

Categorizing Reimbursable Costs: Direct vs. Indirect Expenses

Categorizing expenses with clinical precision is the only way to prevent margin erosion. In a cost-plus environment, your ability to recover costs depends entirely on how they are defined in your contract. Direct costs are typically straightforward; they include raw materials, field labor, and payments to specialized subcontractors. However, with aggregate material prices rising 7% year over year as of April 2026, even these "simple" costs require rigorous tracking to ensure they match the project scope. If a material purchase can't be tied to a specific job phase, it risks becoming an unbillable expense that you must absorb.

Indirect costs are where most disputes occur. These include project-specific supervision, insurance premiums, and small tools. To maintain clarity, many firms look to the Contract Cost Principles and Procedures as a gold standard for defining allowable expenses. Defining these boundaries early prevents the "audit friction" that occurs when a client questions why they're being billed for a superintendent's vehicle or a specific insurance rider. If you find your team struggling to categorize these nuances, you might consider a discovery call to review your current job costing structure.

The most significant danger to your "plus" fee is the unbillable cost. These are expenses that are necessary for the project but don't meet the contract's definition of a reimbursable item. This often includes administrative errors, rework due to contractor mistakes, or general shop supplies that weren't itemized. When these costs pile up, they eat directly into your net profit. Accounting for cost-plus construction contracts requires a proactive approach where every receipt is vetted against the contract's reimbursement clauses before it ever hits the ledger.

Field Labor and Burden Calculations

Labor is often the most scrutinized line item in an audit. You aren't just billing for an hourly wage; you're billing for the "fully burdened" rate. This includes FICA, SUI, FUI, workers' compensation, and health benefits. Transparency here is vital. If your contract allows for burdened labor billing, you must be able to produce the calculations that justify your rates. With the 2026 tax year increase of the 1099-NEC filing threshold to $2,000, managing subcontractor compensation has also become more complex. Daily logs that match timecard entries are your best defense against client skepticism.

Equipment and Consumables

Reimbursing equipment requires a clear strategy for owned versus rented assets. While third-party rentals provide a clean paper trail, internal equipment usage requires a standard rate sheet. This sheet should be pre-approved by the owner to avoid disagreements over "market rates" later. For small consumables like fasteners or adhesives, itemizing every screw is often impractical. Instead, establish a "consumables percentage" or a flat monthly fee for shop supplies within the contract to ensure these small costs don't go unrecovered.

Structuring the 'Plus': Fee Models and Overhead Allocation

Determining the fee structure is a strategic choice that dictates your firm's long-term health. While the "cost" portion of accounting for cost-plus construction contracts covers the field, the "plus" portion must sustain the home office. Many contractors mistakenly view this fee as pure profit. In reality, it must first satisfy your General and Administrative (G&A) expenses before a single cent of net profit is realized. This distinction is critical in 2026, as administrative burdens for documentation have increased alongside material volatility.

To ensure consistency and defensibility, sophisticated firms often align their methodologies with the Cost Accounting Standards (CAS). This framework provides a disciplined approach to overhead allocation, ensuring that your markup is both sufficient and transparent. When you move beyond basic bookkeeping into fractional controller services, you begin to see the fee not as a random percentage, but as a calculated recovery mechanism for your structural integrity.

The Fixed Fee Advantage

Fixed fees provide a stabilizing force in a volatile market. When material costs for copper or steel fluctuate by 25% to 50%, a percentage-based fee can lead to unpredictable revenue swings that complicate your cash flow forecasting. A flat management fee decouples your profit from material prices, which often builds trust with owners. It removes any perception that you're benefiting from rising material costs, positioning you as a partner invested in project efficiency rather than budget expansion.

Percentage Markup and Profit Protection

The percentage markup remains the industry standard for its simplicity and scalability. However, it requires a deep understanding of your true break-even point. The 'plus' should be derived from a rigorous overhead analysis. Change orders play a significant role here; every time the scope increases, your fee should scale proportionally to account for the additional administrative burden. Without this proportional scaling, your profit margin will slowly erode as the project's complexity grows.

Managing a Guaranteed Maximum Price (GMP) requires a heightened level of oversight. Your accounting system must monitor the gap between actual costs and the contract ceiling daily. If the project exceeds the GMP, the "cost-plus" benefit disappears and you transition into a loss-mitigation mode. Incentives, such as shared savings, should be tracked as variable consideration. This ensures your financial reporting accurately reflects potential bonuses only when they are highly probable under ASC 606 guidelines.

Establishing a Bulletproof Audit Trail in QuickBooks Online

A robust accounting system is the only way to survive a client audit without losing your mind or your money. When you're accounting for cost-plus construction contracts, your QuickBooks Online environment must be configured to capture granular data at the point of entry. Generic bookkeeping structures often fail because they don't isolate project-specific costs from general operations. By the time June 15, 2026, arrives and classic reports are retired, your firm needs to be fully transitioned to the modern reporting view to maintain the transparency your clients demand.

The foundation of this audit trail is the 'Billable' checkbox in QuickBooks Online. This single feature creates the technical link between an expense and a customer invoice. When your field team or office staff enters a bill or an expense, marking it as billable ensures that no cost is left behind. To ensure these entries are defensible, you must standardize the attachment of digital receipts to every transaction. If you want to refine this workflow, you can schedule a discovery call to review your QuickBooks configuration.

QuickBooks Setup for Cost-Plus Projects

Isolating cost-plus data requires the use of the Projects feature in QuickBooks Online. This allows you to track labor, materials, and overhead on a project-by-project basis without cluttering your general ledger. You must map every item to the correct expense or COGS account to ensure that your "estimate vs. actual" reports are accurate. For more advanced configurations, see our guide on Mastering QuickBooks for Contractors. Proper mapping ensures that when you run a Profit and Loss by Project, the data is clean enough for a lender or a skeptical owner.

Automating Documentation and Approval

Manual data entry is the enemy of accuracy. Tools like Dext or Hubdoc bridge the gap between field receipts and office records, automating the categorization process and reducing human error. Implementing a digital approval workflow for subcontractor invoices ensures that you never pay for work that hasn't been verified in the field. This level of discipline protects your margins and builds client trust. Learn more about our software training and setup services to build these foundational systems. Transitioning to an automated framework moves your team from basic administrative tasks to high-level financial oversight.

Scaling Cost-Plus Operations with Fractional Controller Oversight

As your firm scales, the volume of data generated by multiple projects can quickly overwhelm a standard bookkeeping setup. You aren't just tracking receipts; you're managing a complex portfolio where margin erosion hides in the gaps between billing cycles. Accounting for cost-plus construction contracts at scale requires shifting from a reactive mindset to a proactive oversight model. This transformation ensures that your financial data serves as a strategic asset rather than a source of administrative stress.

The transition from basic record-keeping to strategic management is often the difference between a firm that survives and one that thrives. A high-level advisor doesn't just record what happened; they analyze why it happened and how it impacts your long-term health. By the time a project reaches its final phase, a controller has already identified potential profit leaks and corrected them, ensuring your fee remains intact. This disciplined approach builds an atmosphere of trust with your clients, who see that their complex needs are understood by experts invested in the project's success.

Why Contractors Outgrow Basic Bookkeeping

Managing several projects simultaneously introduces variables that basic ledger entries simply can't capture. Accurate WIP accounting is essential for cost-plus firms because it reveals the true status of your performance obligations. Without this high-level oversight, unbillable costs can slip through the cracks and quietly eat into your profit margins. A strategic mentor identifies these leaks in real time, preventing the friction that arises when budget overages are discovered too late. This level of clarity is vital for maintaining the structural integrity of your financial reporting.

Partnering for Long-Term Stability

Moving toward long-term stability means building a structural framework that supports growth without sacrificing accuracy. Fractional Controller services provide the specialized expertise needed to transition from reactive billing to proactive cash flow forecasting. This level of management ensures your financials are always lender-ready, which is a critical requirement for securing bonding or financing for larger projects. Reach out to Okie Accounting Group LLC for a strategic financial review to ensure your systems are robust enough to handle the complexities of your growing portfolio.

Building a Foundation for Financial Stability

Success in the 2026 construction market requires more than just skilled craftsmanship; it demands a rigorous approach to financial data. We've explored how precise cost categorization and a disciplined QuickBooks audit trail protect your firm from margin erosion and client disputes. Mastering the mechanics of accounting for cost-plus construction contracts ensures that your business remains transparent, profitable, and ready for any external audit. By shifting from basic administrative tasks to a structural framework of oversight, you move from a state of reactive stress to one of operational clarity.

Okie Accounting Group LLC serves as a strategic partner for firms ready to elevate their financial management. As QuickBooks Online Certified ProAdvisors with a specialized focus on construction and real estate, we provide the national reach and high-level strategy your business deserves. Don't let documentation overhead stall your growth. Scale your firm with strategic Fractional Controller services to secure your long-term stability. You've built the projects; now let's build the systems that protect your success.

Frequently Asked Questions

What is the biggest mistake contractors make in cost-plus accounting?

The most common error is failing to define "allowable costs" with enough precision in the initial contract. This oversight leads to unrecoverable expenses when clients dispute items like small tools, vehicle fuel, or administrative time. Without a clear boundary between direct and indirect costs, these small leaks quickly turn into significant profit bleed that erodes your "plus" fee and creates unnecessary friction during the billing cycle.

Can I use QuickBooks for cost-plus contract tracking?

QuickBooks Online is a powerful tool for this purpose, specifically when you utilize the "Projects" and "Billable" features. This software allows you to isolate every material purchase and labor hour, linking them directly to a customer invoice. Setting up your accounting for cost-plus construction contracts within this framework ensures that your documentation is organized, searchable, and ready for a client audit at a moment's notice.

How do I handle overhead in a cost-plus contract?

Overhead is typically recovered through your fee or a specific labor burden calculation. It is vital to perform a rigorous analysis of your home office expenses, such as rent, utilities, and executive salaries, to ensure your markup is sufficient. Some contractors prefer to bill a fully burdened labor rate that includes taxes and insurance, while others include these indirect costs within a larger percentage-based management fee.

What supporting documents do I need to provide to the owner for billing?

You should provide a comprehensive package that includes vendor invoices, material receipts, and verified timecards for field labor. Owners often demand proof of subcontractor payments and detailed payroll reports to justify burdened rates. Standardizing the attachment of these digital files to every transaction in your accounting system makes this transparency effortless and significantly reduces the time spent addressing skeptical client inquiries during the payment process.

Is a cost-plus contract better for the contractor or the owner?

This contract model is often better for contractors in volatile markets because it transfers the risk of material price spikes directly to the owner. Owners benefit from total financial transparency and the potential for savings if the project is completed under the initial estimate. It creates a collaborative environment where the focus remains on quality and efficiency rather than cutting corners to protect a fixed-price margin.

What happens if a cost-plus project goes over the estimated budget?

The owner is generally responsible for paying the actual costs plus the fee, even if they exceed the original estimate. However, if your agreement includes a Guaranteed Maximum Price (GMP), your firm must absorb any costs that go above that specific ceiling. This is why proactive cash flow forecasting and consistent "estimate vs. actual" reporting are essential for maintaining your firm's long-term health and structural integrity.

How do I account for subcontractor markups in a cost-plus agreement?

You account for these by applying your agreed-upon fee percentage to the total value of the subcontractor's invoice. It is critical that your contract explicitly states whether your markup applies to all third-party labor and materials. Clear language prevents disputes and ensures your financial reporting accurately reflects the management effort and administrative oversight required to coordinate specialized trades on a complex job site.

Should I charge a flat fee or a percentage in my cost-plus contract?

A flat fee provides revenue stability and builds client trust by decoupling your profit from the total project spend. A percentage markup is often more appropriate for projects with a fluid or expanding scope, as it ensures your compensation scales with the increased administrative burden. Your decision should be based on the project's complexity and your firm's specific requirements for predictable cash flow and profit protection.

Comments