Lender Ready Financials for Contractors: The Strategic Checklist for 2026

- Wendy Okie

- 7 days ago

- 12 min read

Lender readiness isn't a frantic cleanup project; it's the natural byproduct of a specialized construction financial infrastructure. You've likely felt the pressure when a lender requests a Work-in-Progress (WIP) schedule that doesn't seem to capture your project's true profitability. It's frustrating to know your business is healthy while disorganized books tell a different story. We recognize that the gap between standard accounting and complex job costing is where many contractors lose their footing and their access to capital.

Building lender ready financials for contractors is about creating the structural integrity that banks demand in 2026. This article provides the exact framework and documentation standards you need to secure capital with confidence. We'll preview how to navigate current hurdles, such as the 100% U.S. citizenship requirement for SBA loans that took effect in March, and how to leverage the permanent 100% bonus depreciation from the OBBBA to strengthen your balance sheet. You're about to gain a clear, strategic roadmap to loan approval and the long-term financial stability your hard work deserves.

Key Takeaways

Understand how lenders evaluate the "Construction Risk Premium" and why your financial reporting must move beyond basic administrative tasks to a project-centric data set.

Identify the specific documentation required for an accrual-basis balance sheet to ensure your assets and liabilities align with lender expectations for 2026.

Master the Work-in-Progress (WIP) schedule as the primary tool for producing lender ready financials for contractors that prove project-level profitability.

Establish a rigorous audit trail using signed contracts and lien waiver management to demonstrate structural integrity and operational control.

Discover how fractional controller services transition your business from reactive bookkeeping to proactive, strategic financial management.

Beyond the Balance Sheet: Why Lenders Demand More from Contractors

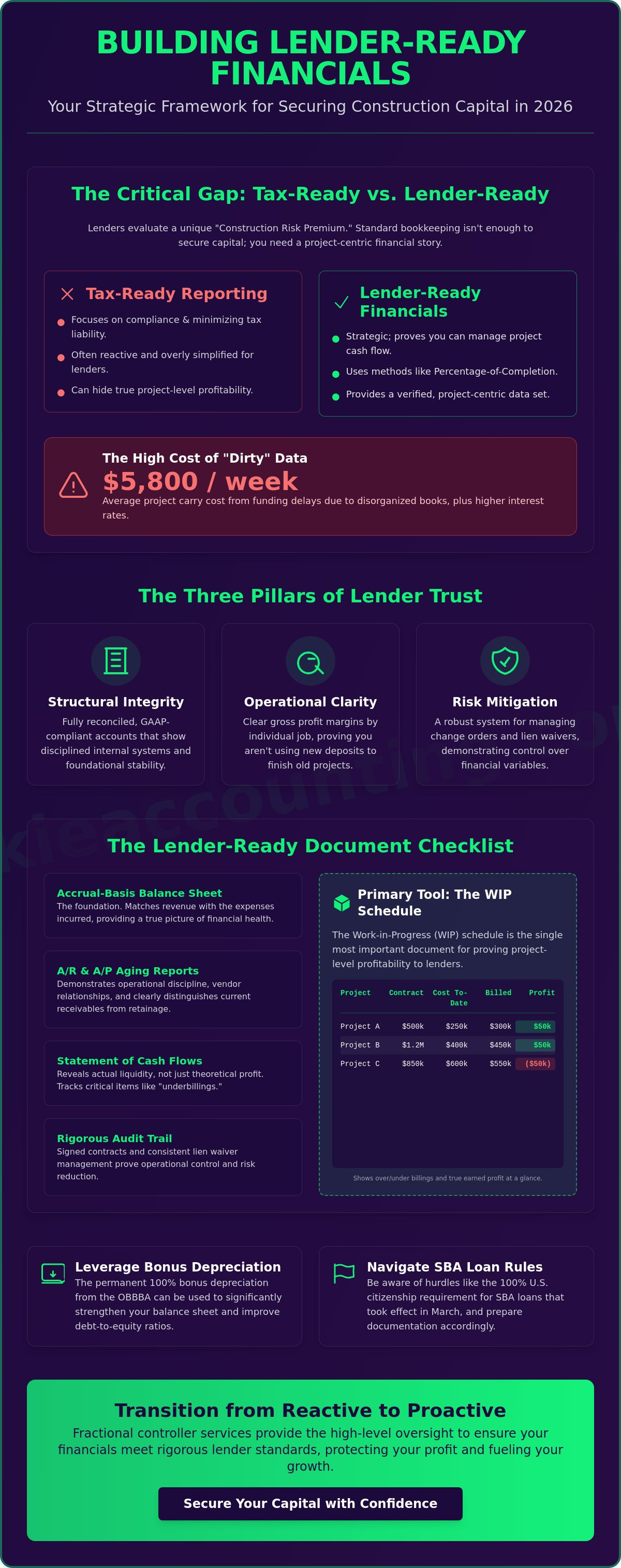

Lender ready financials for contractors represent more than just a clean set of books. While a standard business might get by with a simple Profit and Loss statement, the construction industry operates under a unique "Construction Risk Premium." Lenders view your business through a lens of volatility because revenue is often tied to long-term contracts, fluctuating material costs, and unpredictable labor schedules. To a bank, "lender-ready" means providing a verified, project-centric data set that proves you can manage cash flow through every phase of a build.

There's a critical gap between being tax-ready and being lender-ready. Tax-ready reporting focuses on compliance and minimizing liability; it's often reactive and simplified. In contrast, lender-ready reporting is strategic. It utilizes sophisticated construction accounting methods, such as the percentage-of-completion model, to show exactly how much profit you've earned versus how much you've simply billed. By analyzing historical project data, lenders can predict your future performance with much higher accuracy, reducing their perceived risk and increasing your chances of approval.

The Three Pillars of Lender Trust

Structural Integrity: Your accounts must be fully reconciled and compliant with GAAP. Lenders look for foundational stability that shows your internal systems are disciplined.

Operational Clarity: Can you see your gross profit margins by individual job? Lenders need to see that you aren't "borrowing from Peter to pay Paul" by using one project's deposit to finish another's punch list.

Risk Mitigation: A robust system for change orders and lien waivers is essential. This proves you have control over the legal and financial variables that could otherwise stall a project or trigger a default.

The Cost of "Dirty" Data in 2026

Disorganized books do more than just cause headaches; they carry a heavy price tag. In the current market, funding delays can lead to project carry costs averaging $5,800 per week. When your data is "dirty" or incomplete, lenders often hedge their bets by attaching higher interest rates to your loans to compensate for the uncertainty. If your documentation is messy, you're essentially paying a premium for your own lack of organization.

Precision in your reporting is what secures the most competitive rates. As you scale, fractional controller services can provide the high-level oversight needed to ensure every report meets these rigorous standards. In construction, a lender doesn’t just fund your business; they fund your ability to manage project-level risk. Establishing this trust through lender ready financials for contractors is the most effective way to protect your profit and fuel your growth.

The Financial Statement Checklist: Accuracy Beyond the P&L

A basic Profit and Loss (P&L) statement might satisfy a general tax preparer, but it rarely satisfies a commercial lender in the construction space. Banks require a comprehensive documentation package that proves your business is built on a foundation of accuracy and disciplined oversight. Creating lender ready financials for contractors involves moving beyond simple cash-basis reporting. Lenders demand an accrual-basis balance sheet because it matches revenue with the expenses incurred to generate it, providing a true picture of your financial health at any given moment.

Your Accounts Receivable (AR) and Accounts Payable (AP) aging reports provide a window into your operational discipline. In 2026, lenders pay close attention to retainage, which is the portion of a contract price withheld until project completion. If your AR report doesn't clearly distinguish between current receivables and retainage, a lender might assume your cash is more liquid than it actually is. Similarly, a detailed AP aging report demonstrates that you maintain strong relationships with vendors and subcontractors. This reduces the risk of project stoppages or unexpected liens that could jeopardize a bank's position.

Optimizing the Balance Sheet for Debt-to-Equity

Lenders use your balance sheet to calculate your bonding capacity and overall borrowing power. They scrutinize the ratio between your debt and equity to ensure you aren't over-leveraged for your current volume. It's essential to distinguish between current liabilities, which are due within a year, and long-term debt. This clarity shows you can meet immediate obligations without compromising long-term stability. For a deeper dive into these specific metrics, you can review our guide on Understanding Construction Financial Statements.

Cash Flow Statements: The Contractor’s Pulse

While the P&L shows theoretical profit, the Statement of Cash Flows shows actual liquidity. This is often the most scrutinized document during a lender analysis of contractor financials. You must track "underbillings," which are costs incurred but not yet billed, and "overbillings," which is cash received for work not yet performed. Overbillings can provide a temporary cash cushion, but they also represent a liability for future work. A 12-month rolling cash flow forecast proves you have the foresight to manage these cycles and repay your debt on time.

Building lender ready financials for contractors is a continuous process of system refinement rather than a one-time event. If your current reporting feels more like a "revolving door" than a strategic asset, specialized financial reporting can bridge that gap and provide the clarity you need to scale. Accurate data doesn't just help you secure a loan; it empowers you to make data-driven choices for your firm's future.

Project-Level Visibility: Why WIP and Job Costing are Non-Negotiable

General business accounting looks at the past; construction accounting must look at the future. While the balance sheet and P&L provide a high-level view of your firm's health, they often fail to capture the reality of ongoing projects. For commercial lenders, the Work in Progress (WIP) schedule is the ultimate truth-teller. It's the "holy grail" of reporting because it adjusts for overbillings and underbillings, providing a real-time look at earned revenue rather than just cash collected. Without a professional WIP, your lender ready financials for contractors are essentially incomplete.

Lenders use these reports to identify "profit fade," which is the phenomenon where estimated margins shrink as a project nears completion. If your job costing isn't rigorous, you might report a 15% margin today only to finish at 4% tomorrow. Consistent job costing proves your ability to estimate accurately and manage costs in real-time. This level of transparency builds the quiet confidence lenders need to approve higher credit limits. For a deeper look at protecting your margins through these systems, see our guide on WIP Accounting for Construction.

Elements of a Professional WIP Schedule

Cost-to-Cost Calculations: Lenders want to see percent complete calculated by actual costs incurred versus total estimated costs, not just a guess based on time elapsed.

Contract Integrity: Every report should clearly list the total contract price, including approved change orders, to show the full scope of the project.

Backlog Reporting: This section of the WIP shows your future revenue pipeline. It proves to the lender that your business has the "legs" to support debt service long after the current project wraps up.

Job Costing for Profit Protection

Effective job costing requires tracking labor, materials, and subcontractors at the individual project level. This granular oversight allows you to catch cost overruns before they erode your bottom line. To achieve this, your accounting software must be configured specifically for the industry. Generalist setups won't cut it. For example, QuickBooks Setup & Training ensures your classes and projects are mapped correctly to provide the data lenders demand.

When your system is built on this foundational structure, you stop guessing and start knowing your numbers. You can find more detail on optimizing your platform in our resource on Mastering QuickBooks for Contractors. By providing project-level visibility, you transform your financial statements from a simple compliance hurdle into a strategic asset that secures lender ready financials for contractors and fuels sustainable growth.

The Audit Trail: Documentation Lenders Need to See

Financial statements provide the map of your business's health, but the audit trail serves as the evidence that the map is accurate. When a bank reviews your application, they look for a "structural framework" that supports every number on your balance sheet. Producing lender ready financials for contractors requires a disciplined approach to document management that goes far beyond basic record-keeping. Lenders need to see signed contracts and comprehensive change order logs for every major project. Without these, a bank cannot verify that your reported revenue is legally secured and protected from disputes.

A rigorous lien waiver management system is equally vital. It proves that you are paying your subcontractors and suppliers on time, which mitigates the risk of legal encumbrances on the project. Furthermore, you must provide up-to-date insurance certificates and bonding documents to demonstrate that your firm is adequately protected against operational hazards. If you perform federal or state-funded work, proof of payroll tax compliance and Davis-Bacon adherence is non-negotiable. These documents signal to the lender that your business is managed with professional discipline and long-term stability in mind.

Internal Controls: The "Controller" Layer

Lenders often scrutinize the "who" behind your numbers as much as the "what." They look for a clear separation of duties within your accounting department to prevent errors or fraud. This is where many growing firms struggle, as administrative staff often wear too many hats. Implementing management accounting systems provides the oversight banks demand. A monthly financial review by a fractional controller ensures that your data is scrubbed for accuracy and that your internal controls are functioning correctly. This strategic layer of oversight transforms your books from a simple administrative task into a high-level management tool.

The "Loan Package" Organization

To secure approval, you should present your documentation in a logical, structured package. This organized approach mirrors the methodical systems you use on the job site. Follow these four steps to prepare:

Step 1: Centralize all project-related invoices and receipts to ensure every expense is accounted for.

Step 2: Reconcile all bank and credit card accounts through the current month to prove your cash position is accurate.

Step 3: Verify all sub-contractor compliance documents, including W-9s and insurance certificates, are current and on file.

Step 4: Finalize the WIP report to ensure it matches your General Ledger, providing a unified view of your project performance.

Establishing this level of detail is the most effective way to build lender trust and alleviate the stress of the application process. If you're ready to move from disorganized files to a strategic financial infrastructure, you can schedule a discovery call to discuss how we can help you build lender ready financials for contractors that stand up to the toughest scrutiny.

Building a Strategic Infrastructure with Okie Accounting

Many contractors find themselves trapped in a cycle of "revolving door" bookkeeping. In this reactive state, data is entered to satisfy basic administrative needs, but it's rarely analyzed to drive growth. This lack of oversight often leads to the disorganized books that lenders reject. Transitioning from a general service provider to a strategic partner is the core of our identity. We help you move past simple record-keeping and into a state of strategic oversight by building a comprehensive financial framework designed for the construction industry.

Generalist accountants often struggle with the industry-specific mechanics of WIP schedules, retainage, and job costing. By choosing a specialized partner, you ensure that your lender ready financials for contractors are built using logic that actually fits your business. This specialization doesn't just protect your profit; it transforms you from a business owner caught in the weeds of daily operations into a strategic CEO who leads with data clarity. When your financials are accurate and predictable, you gain the control necessary to make high-level decisions with quiet confidence.

Our Methodology: Profit Protection by Design

Structural integrity is the foundation of our approach. We implement cloud-based systems that allow for real-time project tracking and seamless data integration. This ensures that your job costing and cash flow forecasts are always current, providing a "live" look at your firm's health. Through our Fractional Controller Services, we conduct strategic monthly reviews that go far beyond checking for errors. We analyze your margins, identify potential profit fade, and prepare you for the rigorous questions lenders will ask during your next meeting.

Ready to Scale? Let’s Build Your Foundation

Lender readiness is a journey of continuous refinement. Whether you are a Tennessee-based firm or a national contractor, our team is invested in your long-term stability. We don't just provide reports; we provide the structural systems that prove your business is a safe bet for capital. Accuracy and discipline are the tools we use to help you secure your future and scale your operations without the fear of financial surprises.

It's time to stop worrying about loan rejections and start building a foundation for growth. We invite you to Book your Discovery Call with Okie Accounting Group LLC today. During this session, we'll audit your current financial readiness and identify the specific steps needed to produce lender ready financials for contractors that stand up to any level of scrutiny. Let's move your business from complexity to operational clarity together.

Secure Your Capital and Scale with Confidence

Transitioning your firm from basic bookkeeping to a high-level financial framework is the most effective way to eliminate the fear of loan rejection. By mastering the WIP schedule and establishing rigorous internal controls, you demonstrate the operational clarity that commercial lenders demand. These systems don't just help you pass an audit. They provide the data-driven insights needed to protect your profit margins during every phase of construction. Building lender ready financials for contractors is a strategic investment in your firm's long-term health.

At Okie Accounting, we specialize in the unique mechanics of the construction and real estate sectors. Our fractional controller oversight provides the strategic guidance you need to navigate the complexities of today's market. Whether you're a Tennessee-based firm or a national contractor, we're ready to help you build a foundation for sustainable growth. Your next project deserves a financial partner as dedicated to its success as you are.

Secure your business growth-Book a Discovery Call now

Frequently Asked Questions

What is the difference between tax-ready and lender-ready financials?

Tax-ready financials focus on compliance and minimizing tax liability, while lender-ready financials focus on proving project-level profitability and debt repayment capacity. Lenders require accrual-basis reporting to see earned revenue, whereas tax reports often use cash-basis methods. This distinction ensures the bank sees the true health of your operations rather than just your tax obligations.

Do I need a CPA audit to get a construction loan?

Most commercial lenders don't require a full certified audit for standard construction loans, though they often request "reviewed" or "compiled" financial statements. While our firm doesn't provide certified audits, we ensure your internal books are structured to meet the rigorous standards of bank underwriters. Check with your specific lender to see if they require a CPA's signature on your annual reports.

Why do lenders care about my WIP (Work in Progress) report?

Lenders scrutinize the Work in Progress (WIP) report because it reveals whether you're overbilling or underbilling on active projects. It serves as a truth-teller that adjusts your income statement for revenue that hasn't been earned yet. Without this visibility, a bank cannot accurately assess your liquidity or predict if a project will suffer from profit fade before completion.

How often should a contractor update their financial statements for a lender?

You should update your financial statements monthly to maintain constant lender readiness and internal control. Most commercial loan covenants require at least quarterly reporting, but waiting three months to reconcile accounts can lead to undetected cost overruns. Consistent monthly reporting proves to your lender that you possess the disciplined oversight necessary to manage their capital effectively.

Can I use QuickBooks Online for lender-ready construction accounting?

You can use QuickBooks Online to produce lender ready financials for contractors, provided the software is configured with industry-specific classes and job costing structures. Generalist setups often fail to track project-level data accurately. Strategic QuickBooks setup and training ensure your platform generates the detailed WIP and aging reports that banks demand during the underwriting process.

What are the most common financial mistakes that lead to loan rejection?

The most common mistakes include disorganized books, missing WIP schedules, and inconsistent job costing that doesn't match the general ledger. Lenders also reject applications when they see commingled personal and business funds or unexplained spikes in liabilities. These red flags suggest a lack of structural integrity, making the bank view your firm as a high-risk investment.

How does job costing impact my ability to get a line of credit?

Accurate job costing proves to a lender that you understand your margins and can manage project-level risk. When you can show exactly where every dollar of labor and material is spent, it builds the trust required to secure a larger line of credit. This granular data provides the evidence that your business is a safe bet for expanded capital.

What is a debt-to-equity ratio, and what do lenders look for in construction?

The debt-to-equity ratio measures your total liabilities against your shareholder equity to determine how much of your business is funded by debt. In construction, lenders typically look for a stable ratio that suggests you aren't over-leveraged for your current project volume. Maintaining a healthy balance here is a key component of producing lender ready financials for contractors that secure competitive interest rates.

Comments