Mastering the Chart of Accounts for Real Estate Investors: A 2026 Strategic Framework

- Wendy Okie

- Jun 3

- 12 min read

Your chart of accounts for real estate investors isn't just a list of categories; it's the structural blueprint that determines whether a lender sees you as a professional investor or a high-risk liability. You've likely felt the frustration of staring at a general ledger and still being unable to pinpoint the exact profitability of a single property. In an era where 74% of real estate finance professionals are being asked to do more with less, the confusion of recording security deposits or the fear of an IRS audit over misclassified capital improvements can stall your momentum and your growth.

You deserve a financial system that provides clarity rather than complexity. This framework will help you build a scalable, lender-ready infrastructure that transforms raw property data into strategic growth insights. We'll show you how to leverage 2026 tax advantages like the permanent 100% bonus depreciation under the One Big Beautiful Bill Act (OBBBA). We'll cover the essential categorization for modern portfolios, from handling unrecaptured Section 1250 gains to implementing automated expense tracking that scales with your business.

Key Takeaways

Understand why a specialized chart of accounts for real estate investors is the essential backbone for property-level granularity and long-term scalability.

Learn how to accurately distinguish between Capital Expenditures and Operating Expenses to protect your cash flow and ensure precise asset tracking.

Implement a professional 4-digit or 5-digit block numbering system that allows your financial records to expand seamlessly as your portfolio grows.

Master the "Normal Balance" for each account type to build clean, professional general ledgers that meet rigorous lender standards.

Transition from simple data entry to high-level financial leadership by utilizing your ledger for advanced cash flow forecasting and strategic reporting.

What is a Real Estate Chart of Accounts and Why Does Structure Matter?

A chart of accounts for real estate investors serves as the organizational backbone of your entire general ledger. It's far more than a simple list of names and numbers; it's the DNA of your financial reporting system. To understand What is a Chart of Accounts is to recognize that it functions as a structural framework designed to protect profits and facilitate growth. While most off-the-shelf software provides a generic template, these standard setups often fail real estate professionals. They ignore the property-level granularity required to track individual asset performance, leaving you with a blurred view of your portfolio's health.

When your accounts are structured correctly, they produce "clean" data. This precision is what allows for high-level analysis through fractional controller services. Instead of just recording historical events, your financial system becomes a forward-looking tool. It transforms raw numbers into actionable insights, helping you decide when to divest, when to refinance, and where to allocate capital for the highest return.

The Consequences of a Poorly Designed COA

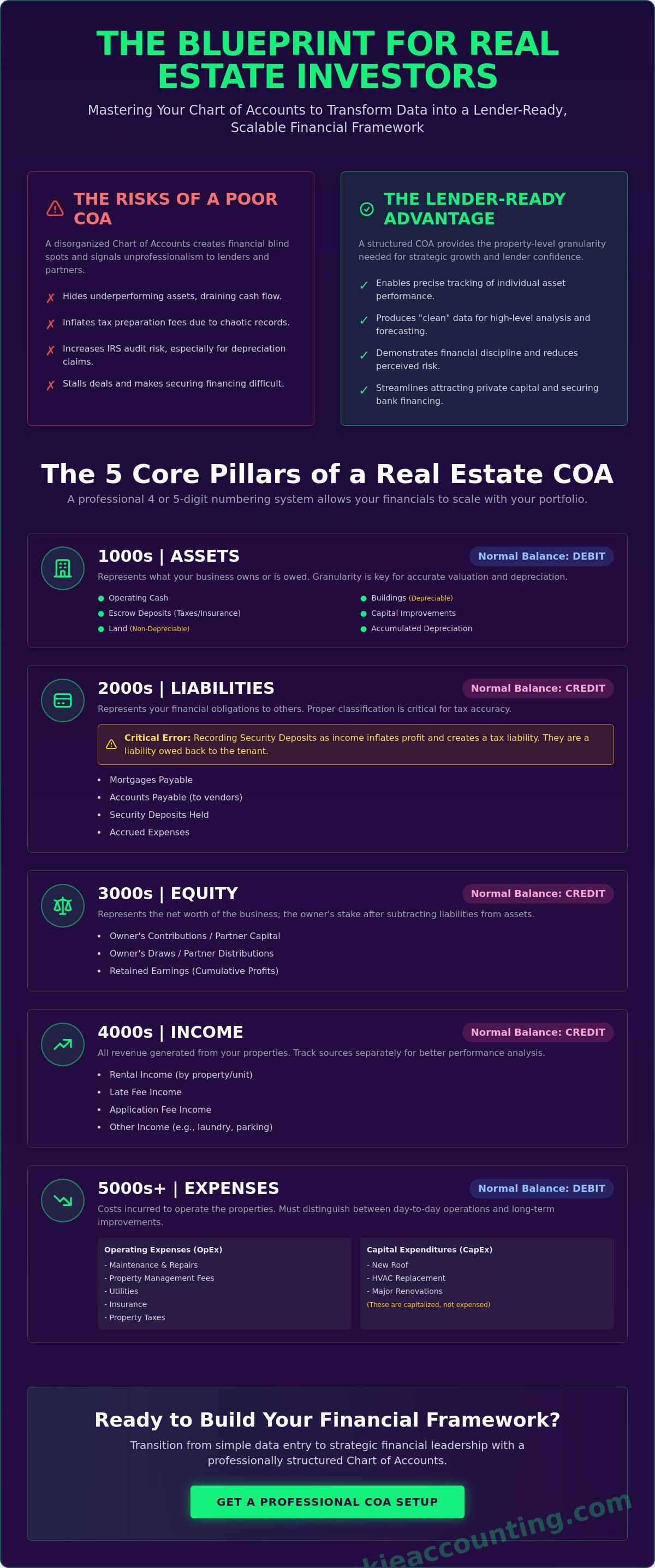

A disorganized chart of accounts creates significant financial blind spots. In a multi-property portfolio, messy accounts often hide underperforming assets. If all your maintenance costs are lumped into a single category, you can't identify which specific building is draining your cash flow. This lack of transparency leads to higher costs during tax season. When financial records are chaotic, your tax professional must spend extra hours unravelling transactions, which results in increased preparation fees. Beyond the cost, disorganized books significantly increase your risk during an IRS audit, especially when trying to justify 2026 bonus depreciation claims. Most importantly, a cluttered ledger signals a lack of professional oversight to potential partners, often stalling deals before they begin.

Lender-Ready Financials: The Investor Advantage

Lenders and private equity partners don't just look at your bottom line; they evaluate the integrity of your reporting. A professional Profit and Loss (P&L) statement should clearly display your Net Operating Income (NOI) and Debt Service Coverage Ratio (DSCR). A structured chart of accounts for real estate investors demonstrates that you manage your business with discipline. It reduces a lender's perceived risk by showing that you have full control over your data. This level of organization is a core component of accounting for real estate investors. By building this foundation, you aren't just keeping track of expenses. You're building a reputation for reliability that makes securing bank financing or attracting private capital a much smoother process.

The 5 Core Pillars of a Real Estate Investor COA

Every professional chart of accounts for real estate investors rests upon five fundamental pillars: Assets, Liabilities, Equity, Income, and Expenses. These categories aren't merely organizational folders; they're the structural supports for your Balance Sheet and Income Statement. To maintain a lender-ready financial infrastructure, you must understand the "Normal Balance" for each. Assets and Expenses carry a natural debit balance, while Liabilities, Equity, and Income carry a natural credit balance. When these are misapplied, your data integrity collapses, making it impossible to produce the clean reports required for high-level fractional controller services.

Consistency across these pillars is what allows for meaningful year-over-year trend analysis. If you shift how you categorize your core accounts, you lose the ability to track your portfolio's trajectory over time. In the 2026 market, where housing price growth has stabilized at a modest 0.3% to 0.4%, your ability to identify small operational efficiencies through consistent data is more valuable than ever.

Assets and Liabilities in Real Estate

Assets represent what your business owns or is owed. In a real estate context, your asset accounts must be granular. You should include specific accounts for Operating Cash, Escrow Deposits held by lenders for taxes and insurance, Land, Buildings, and Accumulated Depreciation. Note that land and buildings must be separated because land does not depreciate, a distinction that is vital for accurate 2026 tax reporting.

Liabilities represent your obligations. This includes Mortgages Payable, Accounts Payable, and, most importantly, Security Deposits. A frequent and costly mistake investors make is recording security deposits as income. These funds are held in trust and represent a liability because they're owed back to the tenant. Treating them as revenue artificially inflates your profit and creates a significant tax liability. If your current system is cluttered with these types of errors, you may find that QuickBooks setup and training is the most direct path to reclaiming control over your data.

Equity, Income, and Operational Expenses

Equity accounts track the owner's stake in the business. This includes Owner Contributions, Partner Draws, and Retained Earnings. Keeping these distinct ensures that you can clearly see how much capital has been reinvested versus what has been distributed. Income accounts should go beyond "Rent" to capture "Other Income" streams that boost your Net Operating Income. This includes Gross Potential Rent, Laundry Income, Late Fees, and Pet Rent. Finally, Operational Expenses (OpEx) cover the daily costs of property management. Your COA should feature dedicated lines for Property Taxes, Insurance, Repairs and Maintenance, and Professional Fees. This level of detail ensures that your financial reporting provides a true reflection of each property's performance.

CapEx vs. OpEx: Categorizing for Tax and Cash Flow

Distinguishing between Capital Expenditures (CapEx) and Operating Expenses (OpEx) is a critical discipline for maintaining an accurate chart of accounts for real estate investors. OpEx includes the daily, recurring costs required to keep a property functional and tenanted. These are fully deductible in the year they occur. CapEx, however, represents investments that either improve a property's value, adapt it to a new use, or significantly extend its useful life. In the 2026 tax environment, getting this right is more impactful than ever. Under the "One Big Beautiful Bill Act" (OBBBA), 100% bonus depreciation is now permanent for qualifying property placed in service after January 19, 2025. This allows you to deduct the full cost of eligible components in the first year, but only if your ledger clearly separates these costs from routine repairs.

To simplify small purchases, investors should utilize the "De Minimis Safe Harbor" rule. This IRS provision allows you to expense items up to $2,500 per invoice or item immediately rather than capitalizing them over decades. Tracking these categories with precision is the only way to ensure your Financial Reporting reflects your true Return on Investment (ROI). Without this distinction, your cash flow forecasting becomes guesswork, as large capital outlays might be incorrectly buried in your operational budget.

The Rehab Phase: Tracking the Basis

During a renovation or "value-add" phase, your accounting must shift from simple expense tracking to basis management. Costs shouldn't hit your Profit and Loss statement immediately. Instead, use "Work in Progress" (WIP) or "Leasehold Improvements" accounts on your Balance Sheet. This approach keeps your project costs organized while the property is being prepared for service. Upon completion, these costs are moved into the Asset value. This granular tracking is vital for establishing accurate depreciation schedules, whether you're using the standard 27.5-year residential MACRS or 39-year commercial schedule. It provides the "clean" data needed for Fractional Controller Services to analyze project profitability.

Repairs vs. Maintenance: The Fine Line

The line between a repair and an improvement is often thin but financially significant. Operating expenses include routine tasks like fixing a leaky faucet, lawn care, or annual HVAC servicing. These are necessary to maintain the property's current condition. Capital expenditures are more substantial, such as a new roof, a full kitchen remodel, or a complete HVAC system replacement. Misclassifying a $15,000 roof as a repair can lead to a massive, incorrect dip in your Net Operating Income (NOI), potentially disqualifying you from bank financing. Conversely, capitalizing a simple repair creates "phantom profits," where you pay taxes on income that was actually spent on maintenance. Correct categorization ensures your Cash Flow Forecasting remains a reliable tool for growth.

Designing a Scalable Numbering and Naming System

Designing a professional chart of accounts for real estate investors requires a forward-thinking approach to numbering and naming. A common error is creating a flat list that becomes unmanageable after only three or four acquisitions. You need a system that remains clean whether you own five units or five hundred. This structural integrity is what separates a hobbyist from a professional operator. By establishing a rigid numbering logic now, you ensure your financial data remains reliable as you scale toward your long-term goals.

Follow these five steps to build your framework:

Adopt a block numbering system: Use 4-digit or 5-digit codes to categorize your accounts by their primary type.

Reserve gaps: Leave space between numbers, such as skipping by 10s, to add future sub-accounts without renumbering your entire ledger.

Standardize naming: Use clear, consistent labels such as "Mortgage Payable: [Property Address]" to keep your records searchable and professional.

Utilize software features: Use "Classes" or "Locations" to track specific properties instead of creating hundreds of individual accounts.

Perform quarterly maintenance: Prune unused or redundant accounts to keep your Financial Reporting concise and actionable.

The Block Numbering Standard

A disciplined numbering system follows a logical flow that mirrors your financial statements. Assets should reside in the 1000-1999 range, covering both current cash and fixed property assets. Liabilities follow in the 2000-2999 range, encompassing short-term payables and long-term mortgages. Equity accounts occupy the 3000-3999 block, while Income and Expenses are assigned to the 4000s and 5000s respectively. This hierarchy makes it easy to spot misclassified transactions at a glance, ensuring your books remain lender-ready and your data stays accurate.

Leveraging Software for Multi-Property Tracking

One of the biggest mistakes in real estate accounting is creating a separate income account for every property in your COA. This leads to a bloated, unreadable Profit and Loss statement that confuses lenders. Instead, your chart of accounts for real estate investors should feature a single "Rental Income" account. To view performance by property, you should leverage the "Classes" feature in your software. This approach is a cornerstone of QuickBooks for contractors and investors who manage multiple projects or units simultaneously. Mastering these advanced categorization tools often requires specialized QuickBooks training for contractors and real estate professionals. To ensure your system is built for long-term health, consider a professional QuickBooks setup and training session to establish these foundational systems correctly from the start.

From Bookkeeping to Strategic Oversight: The Controller Perspective

Transforming your financial data from a static record into a strategic asset requires a shift in mindset. You must move beyond simple data entry and embrace financial leadership. A professional chart of accounts for real estate investors provides the high-fidelity data needed for complex cash flow forecasting and rigorous budget-to-actual reporting. When your ledger is structured correctly, you can see exactly where your capital is working and where it's being wasted. This clarity is essential for making informed acquisition decisions in a 2026 market where home price growth is a modest 0.3% to 0.4% year-over-year. You can't rely on market appreciation alone; you must rely on operational excellence.

Your COA is a living document. It should evolve as your investment strategy shifts from residential flips to long-term commercial holds or niche sectors like logistics hubs. With the global PropTech market valued at up to $54.7 billion in 2026, software provides the tools, but human oversight provides the direction. A clean COA ensures that your financial reporting serves as a reliable map for your business's future.

The Role of Fractional Controller Services

Many investors reach a plateau where basic bookkeeping no longer supports their growth. This is where fractional controller services become a force multiplier. A controller doesn't just record transactions; they interpret the data within your chart of accounts for real estate investors to build internal controls and protect your equity. In an environment where 74% of finance professionals are asked to do more with less, having a strategic partner allows you to stop working in the daily administrative weeds. You can focus on working on your investment portfolio. Controllers use your structured accounts to detect anomalies, which is a vital defense against the surge in digital fraud and business email compromise attempts reported in 2026.

Next Steps for the Growing Investor

If your current financial statements leave you with more questions than answers, it's time to audit your framework. Compare your current categories against the 2026 standards for CapEx, OpEx, and property-level granularity. Foundational errors in your ledger will only compound as you add more units, making future corrections much more expensive. You should consider a professional QuickBooks setup to ensure your classes, locations, and numbering systems are correctly aligned from day one. This investment in your infrastructure pays dividends through lender-ready financials and peace of mind. To build a scalable financial system that supports your long-term vision, contact Okie Accounting Group LLC today to discuss our fractional controller and management accounting solutions.

Securing Your Portfolio’s Financial Future

A precision-engineered chart of accounts for real estate investors is the difference between a portfolio that stagnates and one that scales with confidence. By mastering the distinction between capital improvements and operating expenses, you ensure your business is positioned to capitalize on 2026 tax provisions like 100% bonus depreciation. Adopting a structured numbering system and leveraging software classes provides the clarity needed to present professional, lender-ready financials to any partner or institution. This structural integrity transforms your general ledger from a simple compliance tool into a strategic roadmap.

You don't have to manage these complexities alone. We specialize in real estate investor bookkeeping and provide nationwide fractional controller support to help you transition from administrative tasks to strategic growth. Our cloud-based oversight ensures you have real-time access to the data that drives acquisition decisions. Build your scalable financial infrastructure with Okie Accounting Group LLC and take control of your property data today. Your path to operational excellence starts with a single discovery call.

Frequently Asked Questions

Is a chart of accounts different for residential vs. commercial real estate?

Yes, the primary difference lies in the complexity of income streams and expense recovery. Commercial accounts often include Common Area Maintenance (CAM) reimbursements and longer depreciation schedules of 39 years. Residential accounts focus on gross potential rent and specific tenant fees like pet rent. Both require property level granularity, but commercial investors need additional categories for tenant improvements and specialized utility billing to maintain accurate records.

How do I handle security deposits in my real estate chart of accounts?

Security deposits must be recorded as a liability on your balance sheet, never as income. These funds are held in trust and represent an obligation to the tenant. You should create a specific liability account, often titled Security Deposits Held in Trust, to track these balances. This ensures your profit isn't artificially inflated and protects you from paying unnecessary taxes on money that doesn't belong to the business.

Should I use sub-accounts for every property in my portfolio?

No, you should avoid using sub-accounts for individual properties within your core chart of accounts for real estate investors. Creating separate accounts for every unit leads to a bloated, unreadable Profit and Loss statement. Instead, use the Class or Location tracking features in your accounting software. This allows you to maintain a clean general ledger while still generating detailed reports for each specific asset in your portfolio.

What is the most common mistake investors make when setting up their COA?

The most frequent error is failing to distinguish between repairs and capital improvements. Investors often lunge for an immediate deduction on a large project, like a new roof, which actually needs to be capitalized and depreciated. This misclassification can trigger IRS audits and distort your Net Operating Income. It's vital to apply the De Minimis Safe Harbor rule for items under $2,500 to keep your books compliant and accurate.

How does a well-structured COA help with tax preparation?

A structured COA organizes your data into categories that align directly with tax reporting requirements, such as Schedule E or Form 8825. This organization reduces the time your tax professional spends unravelling messy transactions, which lowers your preparation fees. It also ensures you're ready to claim 2026 tax advantages like 100% bonus depreciation by providing a clear audit trail for all qualifying property components and improvements.

Can I use the standard QuickBooks chart of accounts for real estate?

You shouldn't rely on the generic QuickBooks template because it lacks the specialized categories required for real estate investment. Standard setups don't include accounts for escrow deposits, accumulated depreciation, or specific rental income streams like laundry or late fees. A customized chart of accounts for real estate investors is necessary to track the unique mechanics of property ownership and to produce the lender-ready financial statements professional investors need.

How often should I review or update my chart of accounts?

You should review your chart of accounts at least quarterly to ensure it remains aligned with your current investment strategy. Real estate portfolios are dynamic; you may add new asset classes or change your management structure. A quarterly pruning session allows you to deactivate unused accounts and refine your naming conventions. This proactive maintenance prevents your ledger from becoming cluttered and maintains the integrity of your long-term financial reporting.

What is the difference between a chart of accounts and a general ledger?

The chart of accounts is the master list of all categories used to classify transactions, whereas the general ledger is the actual record of every transaction within those categories. Think of the COA as the organizational filing system and the general ledger as the documents stored inside. A clean COA is the prerequisite for an accurate general ledger. Without a well-defined structure, your ledger becomes a chaotic collection of data that lacks strategic value.

Comments